Jamieson as a firm does not have any specific sector or size focus when it comes to advising management teams. We have worked with leading companies of all sizes, sectors and geographies.

However, within the broad cross section of transactions over the last few years the team here has regularly provided advice and support to teams in the insurance sector, in particular insurance distribution.

Over the years we have advised teams where private equity is selling to private equity and to large listed strategics; we’ve also advised teams raising capital as part of a buy-and-build platform strategy. Examples of past clients include:

- Capital raising support alongside negotiation of associated management terms: PIB (UK), Patriot Growth Insurance Services, Inc (USA), King Insurance (USA)

- Primary buy-out support and advice: Chaucer (UK), EC3 Broking (UK), Endeavour Insurance Services (UK), Miller Insurance (UK), Voogd & Voogd (NED), Charles Taylor (UK)

- Sponsor-to-Sponsor: PIB (UK), Patriot Growth Insurance Services, Inc (USA), CFC Underwriting (UK)

- Sponsor-to-Trade: Aston Lark (UK), Giles Insurance (UK)

We often seen private equity investors following each other into areas of investment opportunity, and this has been no different within the insurance distribution sector over the last few years. This can be led by technological change, strong growth prospects or resilient business models, especially in times of crisis.

During the early stages of the Covid-19 pandemic many businesses held their breath and hoped for the best. While some sectors continue to struggle and are yet to reach pre pandemic levels of trading, others have marched ahead. One sector that has proven to be resilient is insurance distribution – and this resilience continues to be irresistible for private equity.

Across almost all sectors M&A volume plummeted during Q2 2020; but by the latter stages of Q3 and in to Q4 we were seeing a material rebound. In fact, since Q4 2020, Jamieson has seen its highest level of deal activity since opening its doors in 2005.

Insurance Broking \ MGA (“Managing General Agent”) Sector Dynamics

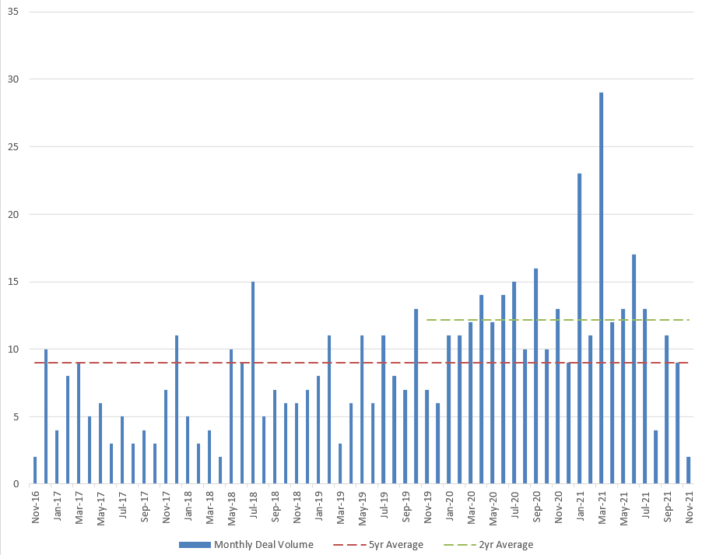

Deal volume in the Insurance Sector, based on MergerMarket data and our own experience, was barely impacted by the pandemic – with every month since January 2020 being above the 5 year average except July 2021. Over the past two years the Insurance sector M&A volume has been 35% above the five-year average.

The insurance industry is attractive in periods of economic disruption because demand for insurance is largely nondiscretionary and claims activity has a low correlation to overall economic activity.

More recently the market has “hardened”, ie the pricing of risk has increased, across a number of lines of business. From a broking perspective this often filters into revenue growth, writing the same policies for an increased premium. MGAs are not always able to retain the same benefits with respect to commissions on re-priced premiums at the smaller end of the spectrum, but larger platforms often have more control over the distribution of their underwriting and therefore more control when defending their commission levels.

And while likely more of a short-term benefit, there has also been a material reduction in Travel, Entertainment and associated general expenses during the past 18 months – thus improving bottom line margins. And brokers, particularly re-insurance brokers, with significant dollar denominated revenue have also benefited from the strength of the dollar against a basket of currencies including the pound.

Alongside the fundamentals outlined above that make for an attractive investment thesis the sector also continues to present value from an M&A perspective.

There remains a beneficial arbitrage in the buy-and-build model with fragmented markets, although in some markets, such as the UK, this is becoming less so with smaller businesses being more available than larger independent privately held businesses.

*Graph sourced from MergerMarket

Broader interest in the Insurance Sector

Although brokers and MGAs have driven a number of the most recent headlines with respect to M&A in the financial and insurance press, it’s not the only aspect of insurance proving popular with investors.

The ancillary service companies remains a fragmented market, this includes businesses focused on claims management, loss-adjusting, third-party administration among others. We worked with the team at Charles Taylor when it was taken private by Lovell Minnick.

Elsewhere in the space Davies Group was recently sold by HGGC to BC Partners and continues to play a significant role in consolidating various services and technology businesses.

Valuation trends in the sector

Since the onset of the pandemic, continued loose monetary policy and associated low interest rates have driven multiples higher across a large number of sectors. This monetary stimulus, combined with sector dynamics driving strong bottom line growth has led to a significant expansion in terms of EV\EBITDA multiples in the last 1-2 years

Without doubt this has supported the increased volume of M&A: strong demand led by a desire to ‘get in to’ the sector has been matched by supply from investors who are hitting return expectations earlier than previously anticipated. Certainly, Aston Lark and Patriot Growth Partners are good examples of this with hold periods of less that 3 years for the investors versus a more common 4-5 years.

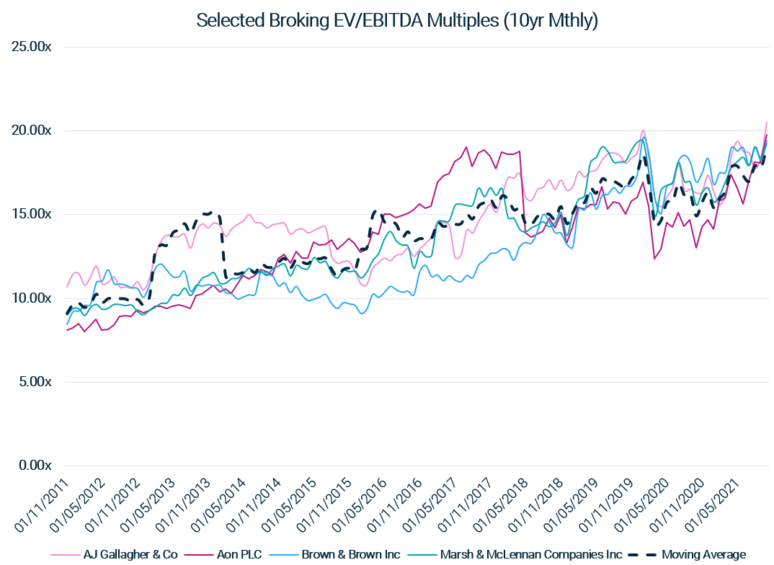

Looking at transaction data on MergerMarket, multiples have increased from an average of ~10x EV\EBITDA in 2007-2011 to an average of ~16x EV\EBITDA during the course of 2021 (with some transactions closer to 17x-18x according to MergerMarket).

Based on research on Eikon (see graph) large public players, such as AJ Gallagher, are currently trading ~3x higher than historic averages.

For individuals leading, or owning, businesses in the sector it’s important to consider where in the value chain they sit. This will help to inform on where the next home for a Company might be – enough scale means being the consolidator, being sub-scale therefore often means being consolidated – within various valuation tiers.

While the large cap consolidators in the US focus on $4m-$5m+ EBITDA businesses (and likewise in the UK) there remains an opportunity for those looking in the sub $1m EBITDA space. We worked closely with Chad King, of King Insurance, who is focused on building a business targeting these smaller family owned companies that should be attractive to the large cap consolidators. BHMS are supporting him in this ambition.

*Graph sourced from Eikon

People are a fundamental ingredient in a majority of insurance broking deals:

What are investors looking for:

- Strong management team with deep sector knowledge

- Strong pipeline for acquisitions or team bolt-ons

- Opportunity to expand internationally

- Disruptive product or strategy (insurtech, fast growing products etc)

Large swathes of the insurance broking market continues to be people orientated. While established and start-up insurtech propositions have reduced this reliance, be that online insurance websites and exchanges, or smartphone apps – for now the higher value products, such as High Net Worth, SME, Commercial Lines, Property & Casualty etc. are very much led by people. This necessitates attractive solutions for retention and incentivisation when making investments into the space.

This desire to look after and motivate the people, combined with a ‘Hot Sector’ and associated competitive processes, has precipitated attractive terms for management teams.

That being said, we are also seeing management teams in the sector rolling over (re-investing) at levels higher than average when compared to the deals across all sectors we have seen in the last 12 months. This is generally because of significant value uplift versus expectations and management taking a view they are rolling the incremental gain and showing commitment to the future upside for the incoming sponsor. What do we mean by this? Conventionally in Europe we might see ‘average’ being ~40% of proceeds net of tax and fees. But on some transactions in hotter sectors we have been seeing management teams accepting / getting comfortable with ~50% of gross proceeds.

What are we seeing in terms of Sweet Equity pots? Larger than average for equivalent sized transactions due to the people nature of the business. There have also been several ‘founder’ CEOs in the sector which can drive higher Sweet Equity pools vs comparable deals where a founder is no longer involved.

Other areas where we’ve seen management teams seeking protections within their terms is with respect to governance, particularly where founders are still involved. It’s a fine balance for the Investor wanting to retain oversight, and the management wanting enough flexibility to operate in what can be a very dynamic market for people and businesses. Finding the right partnership is fundamental to this working relationship and this decision should be a core pillar of a transaction – especially where competitive tension in an auction process aligns pricing.

As discussed earlier, one of the key drivers of investment in the sector is the value from M&A. We are regularly seeing protection against Sweet Equity dilution up to a certain level of follow on capital. This protection can either be used to protect all Sweet Equity shareholders, or be implemented by way of the issue of additional Sweet Equity that can then be used in a bespoke fashion (topping up senior management, incentivising managers of acquired businesses etc).

Being a people orientated type of business it comes as no surprise to see tighter restrictive covenants and leaver provisions. Where individuals are making material sums as part of the transaction this can increase flight risk. Mandated re-investment of meaningful sums (ie 50%) in conjunction with ~2 year restrictive covenants (from cessation of employment) are common place. These restrictions can vary based on the individual participants seniority.

Once terms have been negotiated with the new investors it is important to ensure the management shareholders are also up to speed with the transaction and associated terms. We increasingly are spending a significant amount of time presenting to these broad shareholder groups as part of the educational process. The wealth creation opportunity that may be delivered by a Sweet Equity plan only has the desired retention and incentivisation impact if it is fully understood by participants.

On a number of occasions, once outside of their associated restrictive covenants, we have helped individuals establish new businesses and raise capital in order to support their ambitions in the sector. In this scenario it is important to map out the growth plans of the business and ensure the founder’s / management’s economic and legal terms appropriately cater for the direction of travel.

Additionally, we have helped platforms and businesses in the lower EV range to raise capital (ie sub $150m EV), and implement equity incentive programs in order to deliver the next phase of their growth.

A combination of cheap debt, hardening underlying insurance markets, strong profit margins (which have proven themselves to be robust through the past 24 months), and an inflationary environment makes the distribution sub-sector of insurance attractive. All these factors look broadly set to continue for now.

We’re available and open to working with management teams of all scales of business in Insurance Distribution.

John Greenland has been a Partner of Jamieson since 2014, having joined in 2008. He established the firm’s New York office in 2014 and continues to oversee aspects of the business and work with clients, particularly in Insurance. Most recently he has advised the founders and management teams at Aston Lark, CFC Underwriting, PIB Insurance, Patriot Growth Insurance Services and King Insurance.